The impact of high inflation on individuals’ finances is not something to take lightly, especially in the U.S., because for almost 40 years we have had no experience with such an event and have no clue how to deal with it or how to try to minimize its negative impact. In other countries that is not the case, as low inflation has not been part of their experience, and in some of them, people have become accustomed to dealing with high inflation.

For companies, high inflation is not good for business, even if politicians always use firms’ price increases as scapegoats for their failure to help keep price increases contained. It is true that, in the short term, some firms may benefit more than others from higher-than-expected inflation, especially as inflation accelerates. However, if firms misprice their goods as inflation comes down, which has been the case for the last year and a half, they could lose market share, something that markets will punish severely.

Of course, each industry is different and competitive pressures, or the lack of them, could temporarily benefit those that try to keep prices higher in a disinflationary environment. And in this vein, what we are seeing from the political system is frightening: an increase in protectionist measures such as higher tariffs on imported goods, etc., that are bound to help firms keep prices higher than they would otherwise be if trade was freer.

We know that many of the ‘higher tariffs’ arguments espoused by the political system are intended to gain favor with voters while others are predicated on ‘national defense’ arguments. Some others are lobbied into existence by very powerful industries that benefit from keeping competition ‘contained.’ Let’s face it, in the end, despite the saying “competition is good for business,” it is true only for those that win the competitive race because the rest will be out of business sooner or later. In some sense, one of the true regulatory requirements of a capitalist system, we would argue, is to protect and preserve competition between firms, because this typically guarantees the lowest price possible.

But let’s say that regulation is not effective in keeping a market competitive and domestic firms abuse their pricing power. What should a government do? The answer is, at least in part, to keep imports as free as possible because that will tend to keep prices of domestic companies contained as they risk a flood of imports that could take away their pricing power.

The only problem with this is that this strategy only works when considering goods which, with few exceptions are ‘tradeable,’ that is, they can be exported or imported. However, it doesn’t work with most services, as services, typically, cannot be transacted across countries. That is, if I want to go to a barber, I have to use a neighborhood barber. I cannot go to another country, or even to another state, to get a haircut at a cheaper price. Although I know that my friends in Buffalo, NY, will disagree with me, as they could easily go to Canada for a cheaper haircut!

This is the biggest issue the Federal Reserve (Fed) has today, trying to limit price increases in the service sector, which faces little competition from imports. Hopefully, the Fed will not be inclined to increase interest rates further and it can be patient and wait until it is confident that inflation will remain on its disinflationary path. Remember, as we argued last week, the Fed is already expecting to hit the target of 2% not today, or next year, but in 2026.

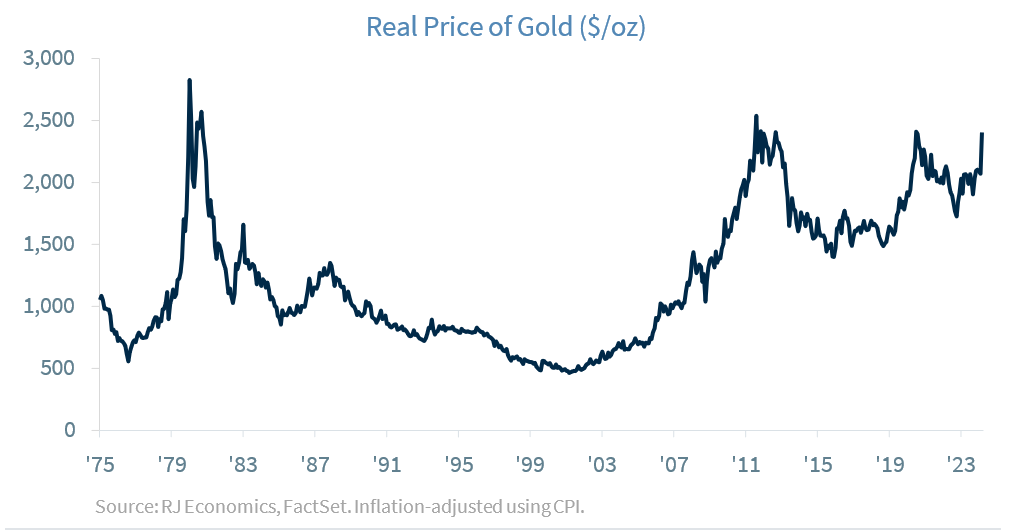

We think gold could be part of a diversified portfolio. But, as with any other investment alternative, sometimes stocks or assets are overpriced. Thus, the first question we should ask is, is this asset overvalued? The second question is, is this asset a productive asset? Let’s take these questions one at a time.

Is gold overvalued or, better still, is gold overpriced? Who knows! Is there any way to know? Maybe. Let’s start with how much it costs, on average, to produce gold. According to an S&P Global report from Q1 2023, the median cost of mining one ounce of gold was $1,239 while the weighted-average mean of mining gold was $1,289.1 Furthermore, according to a report by West Virginia University, 45% of gold is used in jewelry, 45% in investment and finance, and the rest, 10%, is used in industrial processes, with about 75% of industrial use going into the production of electronics.

We would not try to argue against why humans demand gold, as it has been used in jewelry and coinage for centuries. Today, while it has started to be used in industrial applications, its use in coinage is almost nonexistent for a very good reason: debasing.2 Clearly, there is a demand for the metal. However, one of the arguments for gold is that it serves as a store of value, which has been hardly the case over the years.

1 “Large gold miners’ all-in sustaining costs rise in Q1 2023,” S&P Global Market Intelligence, 13 June, 2023, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/large-gold-miners-all-in- sustaining-costs-rise-in-q1-2023-76080833

2 Debasing a coin that contains precious metals means lowering the “precious metal” content of it. This typically happens when the price of the precious metal included in the coin is higher than the extrinsic price of the coin. This is typically called Gresham’s Law.

A second argument in favor of gold is that it has historically protected during periods of high inflation. This was true in the late 70s and early 80s but real gold prices started to surge again during the turn of the century when inflation was very low compared to history.

Furthermore, one of the most successful investors of our times argues that gold is not a productive asset. An article called “Warren Buffet explains gold” argues that “Gold is a poor investment because it doesn’t generate returns or contribute to productivity. However, traders can earn profits by speculating on the price movements of gold in active markets. In most markets, gold does little or nothing.”3

In economics, the value of a good/service is not the same thing as the price of a good/service. One way to understand this is by asking the following questions. First, what would happen to the global economy if gold were to evaporate, i.e., disappear from the face of the earth? Probably nothing will happen. Second, what would happen if water disappeared from the face of the earth? Humanity would disappear. That is, the fact that gold has a high price doesn’t mean that it has a high value, while the fact that water has a low price doesn’t mean it has no value. The value of a good/service is given by its usefulness while the price of a good/service is given by the relative scarcity of that good/service.

Our biggest concern with the ‘dollar doom’ prophecies that abound around the U.S., which we have addressed in previous Weekly Economics reports over the last several years, is that those that sell gold are trying to shift the demand for gold to the right to justify higher gold prices under pretenses, i.e., that the U.S. dollar will disappear, and everybody should rush to buy gold to protect themselves from that event. Even some large wholesalers are selling gold bars in their stores!

If this is what they want to do, the risk for less demand for gold once the demand curve reacts to the fact that the U.S. dollar is not going out of existence, is that there is a potential for a large decline in price.

If that is the reason why you are buying gold, don’t. The U.S. dollar is not going anywhere.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those Raymond James and are subject to change without notice the information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the U.S. Bureau of Labor Studies. Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides a indication of the health of small businesses in the U.S., which account of roughly 50% of the nation's private workforce.

The producer price index is a price index that measures the average changes in prices received by domestic producers for their output. Its importance is being undermined by the steady decline in manufactured goods as a share of spending.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.